ZEBRA-TECHNOLOGIES Earningcall Transcript Of Q2 of 2024

{kind=link}

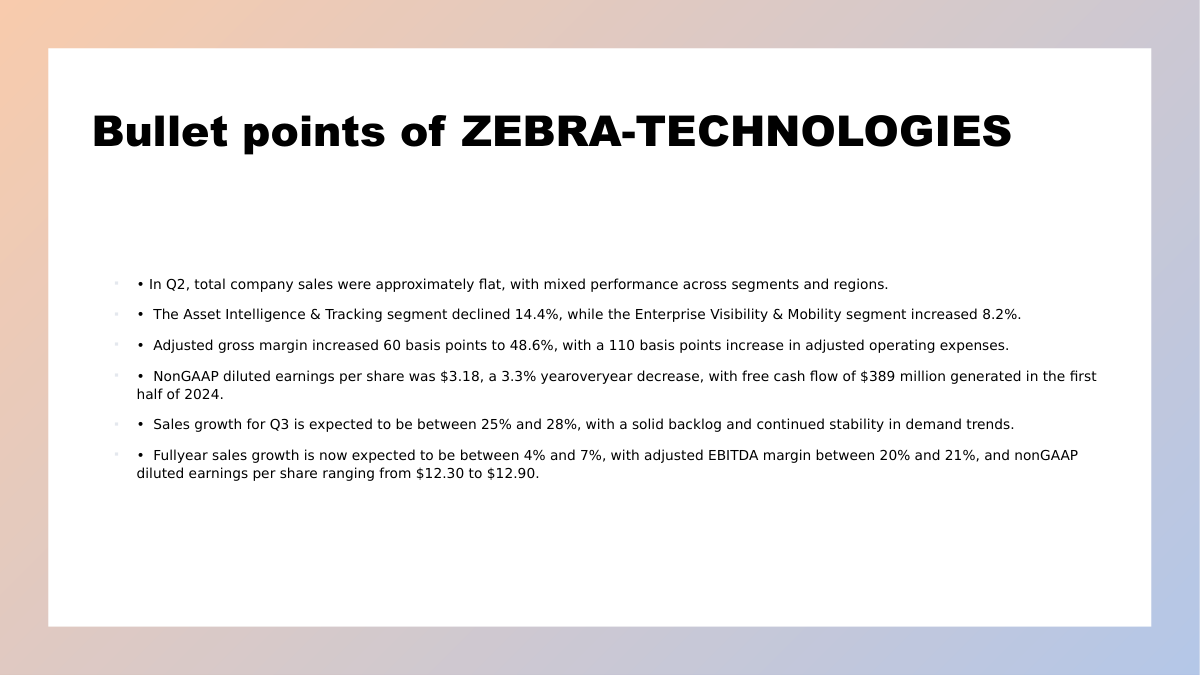

Nathan Andrew Winters -- Chief Financial Officer Thank you, Bill. Let's start with the P&L on Slide 6. In Q2, total company sales were approximately flat, reflecting early signs of momentum demand beyond retail and e-commerce. Our Asset Intelligence & Tracking segment declined 14.4%, primarily driven by printing and RFID on challenging prior year comparisons. Enterprise Visibility & Mobility segment sales increased 8.2% with double-digit growth in mobile computing partially offset by a decline in data capture solutions. We saw modest growth in services and software. Performance was mixed across our regions. In North America, sales decreased 7% with fewer large orders in retail and transportation and logistics, partially offset by strong growth in healthcare. In EMEA, sales increased 10%, driven by mobile computing. In Asia-Pacific, sales declined 3% with continued weakness in China and challenging compares in Australia and Japan, partially offset by growth in Southeast Asia. And sales increased 7% in Latin America led by Brazil. From a sequential perspective, total Q2 sales were slightly higher than Q1, with growth in nearly all product categories as we realized modest improvement in demand throughout the quarter in manufacturing, healthcare, and transportation and logistics. Adjusted gross margin increased 60 basis points to 48.6% as we benefited from cycling premium supply chain costs in the prior year in favorable effects. Adjusted operating expenses as a percent of sales increased 110 basis points. This was driven by normalized incentive compensation expense partially offset by approximately $25 million of incremental net savings from our restructuring actions. This resulted in second quarter adjusted EBITDA margin of 20.5%, a 70 basis point decrease versus the prior year, and a 60 basis point sequential improvement from Q1. Non-GAAP diluted earnings per share was $3.18, a 3.3% year-over-year decrease. Turning now to the balance sheet and cash flow on Slide 7. In the first half of 2024, we generated $389 million of free cash flow as we drove improvements in working capital. We ended the quarter at a 2.4 times net debt to adjusted EBITDA leverage ratio, which is within our target range and we had approximately $1.5 billion of capacity on a revolving credit facility as of quarter end. We diversified our capital structure during the second quarter by issuing $500 million of senior unsecured notes, while retiring a receivable financing facility that matured in May. We also terminated our remaining interest rate swap agreements for $77 million of cash proceeds. We have been prioritizing debt pay down and now have increased flexibility given our lower debt balance and improved cash flow. Let's now turn to our outlook. For Q3, we expect sales growth between 25% and 28% compared to the prior year. This outlook assumes continued stability of demand trends across our major product categories with broad-based growth as we cycle easier compares across the business, including significant destocking activity by our distributors during the second half of last year. We entered the third quarter with a solid backlog and pipeline of opportunities. That said, we are not anticipating an increase in large order activity considering the conversion rates on our pipeline remain lower than historical levels as customers continue to be cautious in what remains an uncertain environment. We would like to see additional momentum in large orders before factoring in a stronger recovery. Q3 adjusted EBITDA margin is now expected to be between 20% and 21%, driven by expense leveraging from higher sales volume with benefits from restructuring actions partially offset by normalized incentive compensation expense. Non-GAAP diluted earnings per share are expected to be in the range of $3 to $3.30. We have raised our guide for the full year, reflecting our second quarter performance and early signs of momentum and demand. We now expect sales growth between 4% and 7% for the year and adjusted EBITDA margin to be in the range of 20% to 21%. Non-GAAP diluted earnings per share are now expected to be in the range of $12.30 to $12.90. Free cash flow for the year is now expected to be at least $700 million. We have been making progress rightsizing inventory in our balance sheet and improving cash conversion. Please reference additional modeling assumptions shown on Slide 8. With that, I will turn the call back to Bill. Bill Burns -- Chief Executive Officer Thank you, Nathan. Zebra is well-positioned to benefit from secular trends that support our long-term growth. These include labor and resource constraints, track and trace mandates, increased consumer expectations, and the need for real time supply chain visibility. We help our customers digitize their environments and automate their workflows through our comprehensive portfolio of innovative solutions, including purpose-built hardware, software, and services. We empower frontline workers to execute tasks more effectively by navigating constant change in real-time through advanced capabilities including automation, prescriptive analytics, machine learning, and artificial intelligence. At our innovation day event in May, we demonstrated how we transform workflows across the supply chain to drive positive outcomes for enterprises across our end market. Our products and solutions are mission critical to enable visibility that consumers and enterprises now expect throughout the entire supply chain. On Slide 11, you will see Zebra solutions can touch a product 30 times from its origination to the point of last mile delivery. Let's briefly walk through the journey with a few high level exams. In manufacturing, our machine vision solutions provide quality inspection and track and trace visibility throughout the process. In a warehouse, our wearable mobile computers, autonomous mobile robots and comprehensive RFID portfolio transform receiving, picking and shipping. As the product arrives at a store, associates are equipped with Zebra software running on our mobile computers to assist customers' stock inventory and fulfill online orders. And when an item is delivered to your home, you receive a notification and picture from Zebra's handheld device verifying on time quality delivery. As you'll see on Slide 12, our customers leverage our solutions to optimize workflows across a broad range of end markets. We empower enterprises to drive productivity and better serve their customers, shoppers, and patients. We are seeing Zebra's competitive differentiation in mobile computing solutions drive wins across our vertical end markets. Customers value the capabilities we embed in the software layer of our devices that they leverage to transform workflows and improve outcome. For example, we secured a mobile computing win with the commercial airline utilizing our mobile package dimensioning solution enabled through AI. Also, a North American retailer will leverage Zebra's work cloud collaboration software on their new wearable mobile computers, connecting their associates to drive better outcomes in their stores. Additionally, we are able to displace consumer cellphones at a European retailer with our mobile computers and Zebra's Identity Guardian solution. It provides multifactor authentication for a shared device environment that brings security, productivity, and convenience to the front line. It is also notable that mobile computing contributed to double-digit sales growth in healthcare. Over the past year, our teams have been successfully selling the benefits of our solutions and clinical mobility that empower caregivers while delivering lower total cost of ownership for hospital systems. We have been displacing consumer cellphones with our devices and there continues to be a long runway of opportunity for equipping more clinicians with mobile computers. In closing, we expect to see broad-based growth in the second half as we cycle much easier comparisons and benefit from momentum beyond retail. We maintain strong conviction in our long-term opportunity for Zebra as we elevate our strategic role with our customers through our innovative portfolio of solutions. Our sales and cost initiatives have positioned us well for profitable growth as our end markets continue to recover. I will now hand it back to Mike. Michael Steele -- Vice President, Investor Relations Thanks, Bill. We'll now open the call to Q&A. We ask that you limit yourself to one question and one follow-up to give everyone a chance to participate. Operator Questions & Answers: |

Zebra-technologies