DOUBLEVERIFY Earningcall Transcript Of Q2 of 2024

{kind=link}

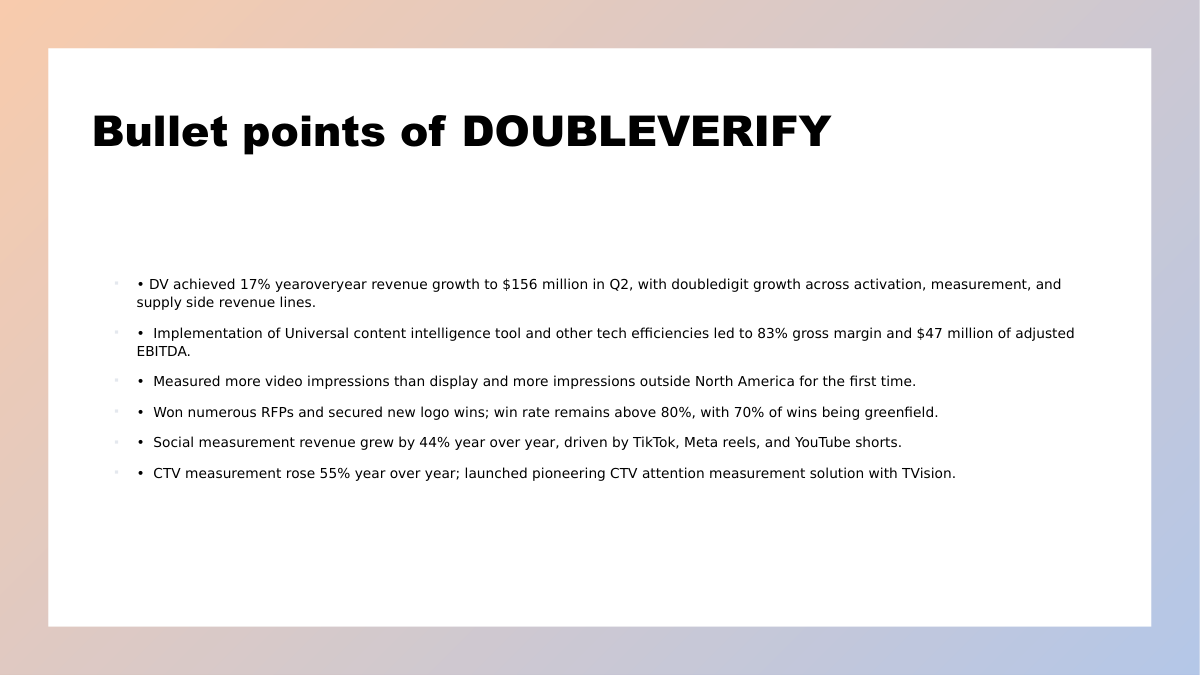

Mark S. Zagorski -- Director and Chief Executive Officer Thanks, Tejal, and thank you all for joining us today. The second quarter was pivotal for DV as we reaccelerated our revenue growth trajectory fueled by ongoing momentum in social and CTV measurement and a sustainable upswing in our supply side platform business, driven in large part by the burgeoning retail media sector. We achieved the high end of our revenue guidance and significantly exceeded our profitability and cash flow expectations. We grew second-quarter revenue by 17% year over year to $156 million with double-digit revenue growth across all three revenue lines: activation, measurement, and supply side. By increasing revenue and reducing our cost of sales year over year through the implementation of our Universal content intelligence tool, a proprietary AI-powered video classification solution, and other investments in technological efficiencies, we achieved an 83% gross margin and $47 million of adjusted EBITDA, representing a 30% adjusted EBITDA margin. Additionally, our net cash from operating activities grew significantly, totaling $36 million for the second quarter. We are at an inflection point in our ongoing evolution as the industry's leading media quality and performance solutions platform. For the first time in DV's history, we measured more video impressions than display impressions and more impressions outside North America than within. These milestones highlight the success of our Verify Everywhere strategy, enabling us to verify every digital ad impression across all channels, formats, and geographies worldwide. As video content, whether short form, long form or CTV becomes the primary way that consumers engage with the Internet and advertisers reach consumers DV has developed the industry's most effective and cost-efficient solutions to verify that those video ad interactions are viewable, secure, and suitable, positioning us perfectly to continue to further capitalize on this trend. Moreover, with digital ad spend outside the United States growing at nearly double the rate of domestic growth per Magna Global, DV has invested in more global resources than any other company in our sector. positioning us to take full advantage of this trend. Building on these achievements, our accelerating momentum is evident in the numerous RFPs we won in the first half of the year. and in an enterprise deal pipeline that has never been stronger with greenfield and competitive opportunities set to fuel our resurgent measurement and leading activation businesses for the next several quarters. Key expansions and new logo wins in the second quarter include Philip Morris and Bacardi across multiple geographies worldwide, Panera in the United States, Anheuser-Busch InBev and British Petroleum in LatAm, Universal Pictures and Subway in EMEA, and Amazon Books, Dyson, Honda Mobility, JTI and Ajinomoto in APAC. Additionally, first-quarter wins such as Haleon and Pepsi have signed up to use key DV products, including ABS and Scibids in additional geographies which will help bolster our activation growth in the future. Our win rate across all opportunities remains above 80%, with 70% of our second-quarter wins being greenfield which we define as wins where the advertiser wasn't using third-party tools for the business that DV won. These new client wins bolster our successful land-and-expand strategy through which we grew the number of advertiser customers generating more than $200,000 over the last 12 months by 16% in the second quarter. Based on our unmatched scale and differentiated solution set, we are also seizing a prime opportunity to gain market share and extend our industry leadership. With Oracle shutting down operations of MOAT and Grapeshot on September 30, we've already attracted interest from many of their advertiser and platform customers who recognize DoubleVerify's differentiated best-in-class capabilities across social activation, Scibids, CTV, and retail media. While we anticipate closing many of these opportunities by year-end, the revenue impact will really kick in, in early 2025 due to the time required for onboarding and ramp-up. Moreover, we expect these customers to grow well beyond 2025 as we typically upsell from measurement to activation between the first to the third year of new contracts. Let's now turn to the progress we've made across all key media environments, social, CTV, Retail Media Networks, and the open web. Our achievements in each environment are the result of DV's growing scale and connectivity and market-defining innovation, all of which are driven by our advancements in AI and automation. We grew our social measurement revenue by 44% year over year in the second quarter of 2024, up from 32% in the second quarter of 2023, driven by growth in short-form video on TikTok, Meta reels, and YouTube shorts. Our independent verification of social feeds has become increasingly important to our enterprise partners navigating the high-value, high-engagement, yet sometimes challenging content in social media. Since launching our brand safety and suitability measurement solution on Meta early this year, we've successfully sold our measurement solution to over 30 advertisers who had never activated DV on Meta before. We're excited to build on this upsell momentum over the coming months and quarters. On YouTube, we now provide comprehensive brand safety and suitability reporting for Google's latest high-performance ad solutions. With our expanded coverage, advertisers can now measure Performance Max, an AI-powered campaign tool that optimizes in real time to maximize conversions and budget efficiency. Additionally, our reporting now includes Demand Gen, a Google Ads solution designed to attract and convert customers through visually engaging and relevant campaigns. Our partnerships with Pinterest and Reddit are also growing, and we've launched global brand safety and suitability measurement across both platforms and multiple languages. Using DV's AI-powered three Universal content intelligence we integrate advanced image, audio, and text analysis to provide accurate media quality measurement and robust brand protection. These strategic expansions and technological advancements across Meta, YouTube, Pinterest, and Reddit highlight our commitment to grow and scale our social media offerings, and we are just at the start of our growth in social measurement. In 2023, DV measured less than 5% of all U.S. social impressions according to our analysis of the eMarketer data, highlighting the vast opportunity to expand our measurement footprint in a rapidly growing media environment that accounts for over 60% of global digital ad spend ex search. Moreover, we're increasingly excited about the potential for social prescreen activation applications in the social media sector. Although we are in the early stages of pre-screen activation growth on social platforms, we believe this area could become a significant growth driver for DV, similar to how activation solutions like ABS have driven our growth in the open web. A great indicator of the potential for pre-bid solutions in social is our free screen solution for YouTube. With close to 100 customers, including nearly 30 of our top 100 customers, this solution drove 30% year-over-year growth in social activation revenue in the second quarter. Currently, we are the only verification platform capable of closing the loop for advertisers on social media with aligned pre- and post-bid solutions. And our coverage is just beginning. We are actively developing ABS-like pre-bid applications across three additional major social platforms where we see an activation opportunity potentially as large as what we have achieved in the open web. Shifting to CTV. We grew our second-quarter CTV measurement impression volumes by 55% year over year. We partnered with a leading streaming network to launch a groundbreaking program-level measurement solution for advertisers on OTT devices, including CTV. Our initial test of this solution with Cox Automotive via OMG showcased granular program-level insights for the first time, providing invaluable transparency in the often-opaque world of CTV advertising. We plan to expand this offering to more advertisers and streaming publishers in the coming months. Similar to our status in social, we are also in the early stages of our growth in CTV verification and have much room to expand. In 2023, DV advertiser engagement measured less than 20% of all U.S. CTV impressions based on our analysis of eMarketer data, revealing another significant opportunity to expand our measurement volumes and build our CTV market position. In addition to CTV verification, we are also now in market with a pioneering CTV attention measurement solution in partnership with TVision Advertisers can drive ROI by measuring attention in CTV to better understand ad placement and effectiveness. According to the IAB, only 30% of advertisers have full transparency of CTV ad placements and only 34% of CTV ads receive more than two seconds of active eyes on screen attention. DV's Authentic Attention solution powered by impression-level DV data and TVision viewer engagement data enhances visibility into ad performance across CTV publishers and apps, enabling strategic optimizations and preventing wasted ad spending. Reflecting the growing importance of attention metrics, DV Authentic Attention increased measurement impression volumes by approximately 300% year over year in the second quarter, with over 200 advertisers using DV Authentic Attention this year. Although the scale of our attention business remains relatively small, its impact on our ability to differentiate our platform en route to closing and expanding enterprise deals has been significant. With the Oracle-fueled expansion of RFP opportunities currently in play, having differentiators like Authentic Attention will play an important part in driving a highly favorable win ratio. Moving to Retail Media Networks. Our retail media supply side solutions delivered over 50% revenue growth, significantly contributing to our overall supply side growth rate of 26% year over year. We provide comprehensive solutions to retail media platforms, ensuring platformwide fraud protection and brand safety standards. Additionally, we empower platforms to make a real-time and long-term viewability optimizations across all inventory with insights based on our MRC-accredited measurement. Furthermore, we enable platforms to leverage DV's contextual classifications to curate premium contextual segments of inventory. Led by our partnerships with leading retail media platforms such as Amazon and Walmart, our global reach and connectivity in retail media continue to expand. DV's measurement tags are now accepted on over 100 key global retail media networks and sites, including 15 of the top retail media platforms and 88 major retailers. More than one-third of these partners support DV measurement on their owned and operated as well as off-site inventory. Within the supply side, we also signed DailyMotion, an online video-sharing platform as well as several high-profile publisher customers such as Ziff Davis, Complex Networks, and The Independent. Finally, turning to our open web activation products. Several factors give us confidence in a stronger growth trajectory. First, our measurement momentum and historical subsequent activation upsell motion indicates renewed strength in our activation business in the future. Second, we expect ABS's growth to improve in the second half as new customers ramp up on activation and ABS. From a long-term perspective, while over 90 of our top 100 customers use ABS, close to 40% of their business lines have yet to adopt it, and there is even greater potential for growth among our top 500 customers. Third, given the strong interest from advertisers and agencies, we anticipate Scibids AI will exceed our expectations in the second half of the year and beyond. Expansion of our activation and measurement solutions across the open web remains a key part of our Verify Everywhere strategy as advertisers continue to lean into the efficient performance opportunities that the open web entails, particularly in light of the recent change in position from Google regarding cookies. We believe that Google's announcement to step back from blocking third-party cookies by default on Chrome will instill confidence in buyers to spread across programmatic channels and create additional growth opportunities for our advertiser, platform, and publisher customers. We also see the open web as a beneficiary of the expected increase in political spending in the latter half of the year, and we plan to support that via our recently launched authentic news initiative, which is an investment in market education and product development that will create a more flexible, transparent way for advertisers to support open web news content while still protecting brand equity. In conclusion, the second quarter was an important positive inflection point for DoubleVerify marked by accelerated revenue growth and significant expansion milestones. We won numerous RFPs, strengthened our enterprise pipeline, and continue to innovate across social, CTV, and retail media networks. With vast opportunities in social with CTV measurement, anticipated improvement in activation and ABS, and strong momentum for Scibids AI. We are confident in our near- and long-term growth prospects. We remain committed to delivering unparalleled value and driving sustained growth for all of our stakeholders and look forward to updating you on our ongoing progress and achievements. With that, let me turn the call over to Nicola. Nicola Allais -- Chief Financial Officer Thanks, Mark, and good afternoon, everyone. Our second quarter results achieved the high end of our revenue guidance and exceeded our adjusted EBITDA expectations driven by double-digit growth across all three of our revenue lines: activation, measurement, and supply side. Total revenue grew 17% in the second quarter to $156 million. Advertiser revenue increased 16% in the second quarter, driven by higher volumes. Media transactions measured or MTMs, increased 22% year over year, while measured transaction fees or MTFs declined 5% year over year due to product and geographic mix. As expected, premium-priced activation represented a smaller portion of total revenue compared to the prior year period. More significantly, as Mark mentioned, the second quarter of 2024 marked the first time DV impressions outside North America represented just over half of DV's total measurement impressions with measurement impressions within North America growing over 20% and measurement impressions outside North America growing over 50%. While we expect MTFs to remain stable on a per-product basis, we anticipate overall MTFs to reflect the impact of a greater shift toward measurement impression volumes. Within measurement, we foresee a continued increase in international pressure driven by DV's global client expansion and international market share gains. Our profitability and margins remain robust, and we continue to be strategically focused on volume-led revenue growth. DV has significant potential to continue to expand across international markets and particularly on social media platforms. By initially engaging customers through measurement, we can upsell our premium-priced activation solutions. Measurement data feeds into our activation solutions, helping advertisers optimize their media spend effectively. We aim to capitalize on this opportunity in social media where prescreen MTFs are nearly triple the price of measurement MTFs. Activation revenue increased by 12% compared to the prior year. All four activation solution groupings, ABS, Core Programmatic, Social Activation, and Scibids contributed to the second quarter growth. ABS, which accounted for 53% of activation revenue this quarter grew 7% year over year. Similar to the first quarter, the group of slow-starting retail and CPG advertisers who are heavy users of ABS delivered an uneven spend pattern that continued to impact ABS growth in the second quarter. We achieved solid ABS upsell momentum with 65% of our top 500 customers activating the product in the second quarter, up from nearly 60% a year ago. Additionally, new advertisers such as Haleon and Pepsi have activated ABS and are expected to expand their use of the product. Scibids continued to perform in line with plan in the second quarter. Based on customer usage and adoption patterns, we anticipate an accelerated growth trajectory for Scibids in the second half of the year. And lastly, our prescreen social activation solutions achieved a robust 30% year-over-year growth rate in the second quarter. Turning to measurement. Revenue increased 22% year over year, primarily driven by existing customer expansion on social. Social revenue increased 44% year over year and represented 49% of measurement revenue in the quarter. Growth in social measurement continued to be led by Meta and YouTube which combined accounted for approximately 80% of our second-quarter social measurement revenue with TikTok being a distant third. Global expansion of new deals and growth in social media measurement drove international measurement revenue, which increased 29% compared to the prior year and represented 29% of total measurement revenue, up from 28% in the second quarter of 2023. Finally, supply side revenue grew 26% in the second quarter, driven primarily by greater usage of DV Solutions on retail media platforms such as Amazon. Shifting to expenses. Cost of revenue decreased by less than 1% year over year in the second quarter due to savings resulting from the company's migration to cloud services and to efficiencies gained from video classification costs. These cost reductions were partially offset by the growth in activation revenue, which led to increased partner costs from revenue-sharing arrangements. Revenue less cost of sales reached 83% in the second quarter, exceeding our expectation of 80% to 82%. For the second half of the year, we anticipate maintaining revenue less cost of sales at the higher end of the 80% to 82% range. Research and development expenses increased due to continued investment in AI and machine learning engineering resources. As mentioned last quarter, we also invested in additional sales and marketing resources, including technical programmatic analysts to promote and sell our latest product launches, such as Scibids. These investments will contribute to sales and marketing expense growth throughout the year. General and administrative expenses remained relatively stable year over year as our growing scale helps leverage this operating expense line effectively. Adjusted EBITDA of $47 million in the second quarter represented a 30% margin and was ahead of expectations due to both higher revenue and lower cost of revenue. We delivered net cash from operation of approximately $36 million, up from $11 million in Q2 '23, primarily due to strong cash collections. Capital expenditures were approximately $7 million compared to approximately $3.5 million in Q2 2023. We ended the quarter with approximately $256 million of cash on hand, including investments in treasury bills with maturities over three months, total cash and short-term investments were $339 million. In the second quarter, we repurchased 1.4 million shares of common stock for $25 million. Following the quarter's end, we repurchased an additional 1.3 million shares for an additional $25 million. As of July 30, we had $100 million authorized and available for further repurchases. Our approach to share repurchases will remain balanced, taking into account market conditions and other capital priorities, including investing in our core business for sustained long-term growth and in acquisition that can accelerate our product road map and our market expansion. Turning to guidance. We are raising the midpoint of our full-year guidance based on our second-quarter performance and remain confident in our anticipated growth reacceleration in the second half of the year. We expect third-quarter revenue to range between $167 million and $171 million, which represents a 17% year-over-year growth at the midpoint. We expect third-quarter adjusted EBITDA to range between $49 million and $53 million, which represents a 30% margin at the midpoint. For the third quarter, we expect stock-based compensation to range between $23 million and $26 million and weighted average diluted shares outstanding to range between 172 million and 175 million shares. For full year 2024 guidance, we expect revenue to range between $667 million and $675 million, which represents a 17% year-over-year growth at the midpoint, and we expect adjusted EBITDA to range between $206 million and $214 million, which represents a 31% margin at the midpoint. We expect the second half of the year to contribute approximately 56% of full-year revenue, broadly in line with last year's second-half performance. Our outlook for the second half reflects an acceleration to 18% revenue growth, up from 16% achieved in the first half. This is driven by multiple growth vectors, including sustained social revenue growth accelerating momentum in Scibids, successful conversion of our high-confidence pipeline into wins, and continued growth in supply side, particularly within retail media platforms. We have not changed our outlook or expected impact from the cohort of six large retail and CPG advertisers that we previously mentioned as having uneven spend patterns in this year. As noted last quarter, the reduced spending from these advertisers is due to specific issues within each company. Other retail and CPG advertisers are performing at or above expectations. Finally, our second half guidance does not factor in meaningful incremental revenue from increased adoption of our measurement solution on Meta, nor does it assume increased contribution from former most advertiser and platform customers to account for the time required to onboard and ramp. We expect these two opportunities to be contributors in 2025 and beyond. In conclusion, we achieved a strong second quarter with double-digit revenue growth across all three revenue lines, robust profits, and substantial cash flow. We ended the quarter with zero debt and $339 million in cash on hand and short-term investments and are focused on executing to drive strong growth momentum for the second half of the year. And with that, we will open the line for questions. Operator, please go ahead. Operator Questions & Answers: |

Doubleverify