COCA_COLA Earningcall Transcript Of Q2 of 2024

{kind=link}

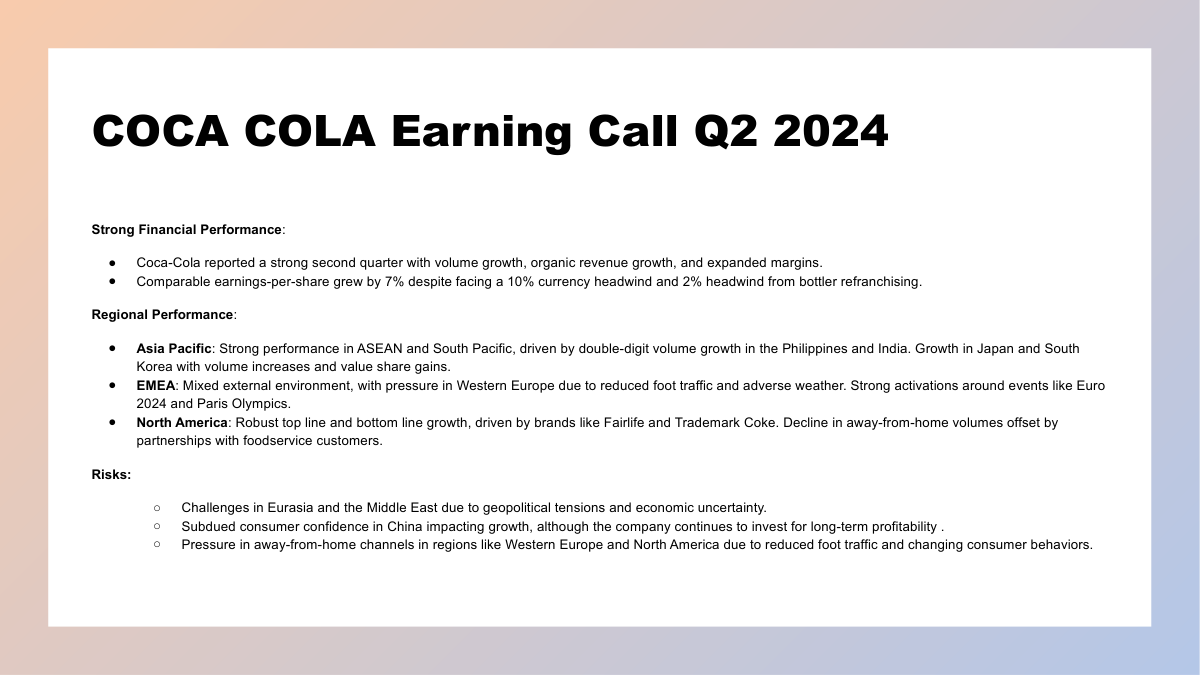

John Murphy -- President and Chief Financial Officer Thank you, James, and good morning, everyone. In the second quarter, we delivered strong results. We grew organic revenues 15%. This consisted of 2% unit case growth. Concentrate sales were ahead of volume by four points, driven primarily by timing of concentrate shipments and some disruptions in the global supply chain that we partly expect to reverse next quarter. Our price/mix growth of 9% in the quarter was primarily driven by two items: one, approximately five points of intense inflationary pricing across a handful of markets to offset significant currency devaluation and two, an array of pricing and mix actions across our markets. Excluding the impacts from concentrate shipment timing and pricing from markets with intense inflation, Organic revenue growth during the quarter was at the high end of our long-term growth algorithm. Comparable gross margin was up approximately 200 basis points, driven by underlying expansion and the benefit from bottler refranchising partially offset by currency headwinds. Comparable operating margin expanded approximately 120 basis points. Comparable operating margin expansion was less than comparable gross margin expansion due to less benefit from bottler refranchising and greater currency headwinds to comparable operating margin. Putting it all together, second quarter comparable EPS of $0.84 was up 7% year over year despite 10% currency headwinds and 2% headwind from bottler refranchising. Free cash flow was approximately $3.3 billion, down approximately $700 million versus the prior year. due to higher tax payments, cycling working capital benefits from the prior year and higher capital expenditures. We continue to take actions to achieve a fit for purpose balance sheet that will best support our growth agenda. During the quarter, we raised approximately $4 billion in cash by issuing long-term debt for general corporate purposes. This may include pre-funding upcoming payments related to the IRS tax case and the Fairlife contingent consideration. With respect to our IRS tax case, which we continue to vigorously defend. We're making progress to our next steps, and we expect we will be able to move forward an appeal by the end of the year. Given the continued outperformance of Fairlife, we recorded a charge of $1.3 billion during the quarter. Our estimated final payment related to this acquisition is $5.3 billion, which will be made in 2025. We are encouraged by Fairlife's performance and the value it has created for our company. So far this year, we've realized nearly $3 billion in gross proceeds from bottler refranchising and streamlining our equity investments. We'll continue to prioritize higher growth businesses and take passive capital off the table. Return on invested capital is 24%, up approximately five points from three years ago. Our balance sheet is strong, as demonstrated by our net debt leverage of one and a half times EBITDA which is well below our targeted range of two to two and a half times. We have ample capacity to pursue our capital allocation agenda, which prioritizes investing to drive further growth, continuing to support our dividend and staying dynamic, agile and opportunistic. As James mentioned, we're proactively managing our portfolio to deliver on our commitments. Our updated 2024 guidance reflects the momentum of our business in the first half of the year. and our confidence in our ability to execute on our plans during the second half of this year. We now expect organic revenue growth of 9% to 10% and comparable currency-neutral earnings-per-share growth of 13% to 15%. Bottler refranchising is still expected to be a four- to five-point headwind to comparable net revenues. And we now expect a one- to two-point headwind to comparable earnings per share. Based on current rates and our hedge positions, we now anticipate an approximate five- to six-point currency headwind to comparable net revenues and an approximate eight- to nine-point currency headwind to comparable earnings per share for full year 2024. This increase in currency headwind is driven by a small number of intensive treasury markets, while the rest of the currency basket is relatively neutral to our results. All in, we now expect comparable earnings-per-share growth of 5% to 6% versus $2.69 in 2023. There are some considerations to keep in mind. We expect unit cases and concentrate shipments to be relatively in line with each other for the full year 2024. Please keep in mind there are two extra days in the fourth quarter. Taking everything into consideration, we expect earnings growth during the remainder of 2024 will be weighted toward the fourth quarter. To summarize, we're encouraged by our track record and the underlying momentum of our business. Our system remains incredibly focused and motivated to drive growth. We're continuing to drive quality top line growth, expand margins grow comparable earnings per share and improve the return profile of our business. And we're confident we will deliver on our guidance and longer-term objectives. With that, operator, we are ready to take questions. Questions & Answers: |