CINCINNATI-FINANCIAL Earningcall Transcript Of Q2 of 2024

{kind=link}

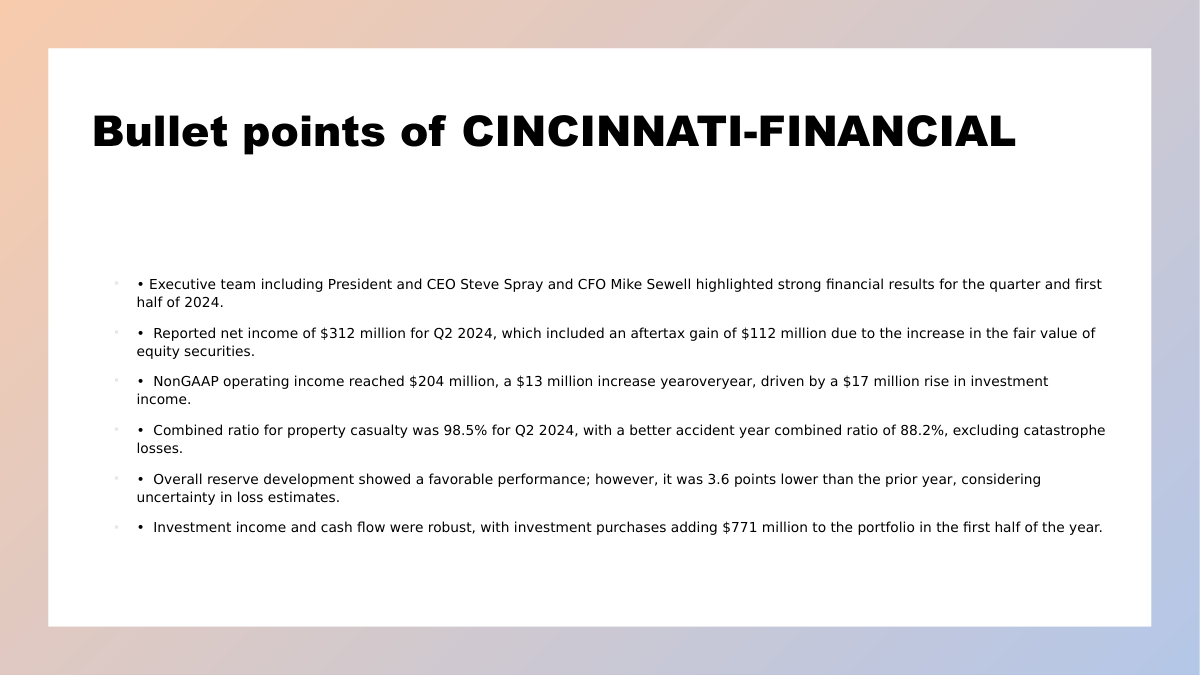

from executive vice president and chief financial officer, Mike Sewell. After their prepared remarks, investors participating on the call may ask questions, At that time, some responses may be made by others in the room with us, including executive chairman, Steve Johnston; chief investment officer, Steve Soloria; and Cincinnati Insurance's chief claims officer, Mark Schambow; and senior vice president of corporate finance, Theresa Hoffer. Please note that some of these matters to be discussed today are forward-looking. These forward-looking statements include certain risks and uncertainties. With respect to these risks and uncertainties, we direct your attention to our news release and to our various filings with the SEC. Also, a reconciliation of non-GAAP measures was provided with the news release. The statutory accounting data is prepared in accordance with statutory accounting rules and therefore is not reconciled to GAAP. Now, I'll turn it over to call to Steve. Steve Spray -- President and Chief Executive Officer Good morning and thank you for joining us today to hear more about our results. We had a good quarter and first half of the year. In addition to our strong financial performance, recent travel to meet with agents reinforced my excitement about the future. Agents are quite enthusiastic about doing business with us, citing our responsiveness as we answer the call, both literally and figuratively, to help them navigate this challenging insurance market. While picking up the phone is part of our culture, the confidence we have in our expertise in Cincinnati's Financial's strength lets us continue growing profitably, delivering insurance solutions for our agents and their best clients. Net income of $312 million for the second-quarter of 2024 included recognition of $112 million on an after-tax basis for the increase in fair value of equity securities still held. Non-GAAP operating income of $204 million for the second quarter was up $13 million from a year ago. Investment income continued to grow nicely and contributed $17 million of the increase. The 98.5% second-quarter 2024 property casualty combined ratio was 0.9 percentage points higher than the second quarter of last year and included a decrease of 0.8 points for catastrophe losses. That brought the first-half combined ratio to 96.1%, a nice place to be as we head into the second half of the year. Typically, the end of the year tends to be better than the beginning, in part due to the catastrophe loss ratio averaging about two points better in the second half based on the past 10 years. Our 88.2% accident year 2024 combined ratio before catastrophe losses improved by 2.2 percentage points compared with accident year 2023 for the second quarter, and was 0.7 points better on a six-month basis. Once again, overall reserve development on prior accident years was favorable. Although it was 3.6 points lower than a year ago, as we continue to consider uncertainty regarding ultimate losses and remain prudent in our reserve estimates until longer-term loss cost trends become more clear, we are entering the second half of the year with confidence and optimism. In addition to improved accident year results and an overall combined ratio for the first half of 2024, that was better than last year's first half, we are pleased with measures -- with other measures regarding our operating performance. We had strong second-quarter premium growth and believe it is profitable growth. We continue to use pricing segmentation by risk, plus average price increases, along with careful risk selection to help improve our underwriting profitability. Those efforts plus others are bolstering our progress in managing elevated inflation effects on insured losses. Agencies representing Cincinnati Insurance produced another quarter of profitable business for us, and we continue to appoint additional agencies where we see a appropriate expansion opportunities. Our underwriters continue to do excellent work as they emphasize retaining profitable accounts and managing ones that we determine have inadequate pricing based on our risk selection and pricing expertise. Estimated average renewal price increases for the second quarter were again at healthy levels with commercial lines near the low end of the high single-digit percentage range, excess and surplus lines in the high single-digit range, personal auto in the low double-digit range, and homeowner in the high single-digit range. Our consolidated property casualty net written premiums grew 14% for the quarter, including 12% growth in agency renewal premiums and 34% in new business premiums. Next, I'll briefly highlight operating performance by insurance segment, focusing on second-quarter premium growth and underwriting profitability compared with a year ago. Commercial lines grew net written premium 7% for the second quarter with a 99.1% combined ratio that increased by 2.2 percentage points and included prior accident year reserve development that was less favorable by 2.9 points. Personal lines grew net written premiums 30% including growth in middle market accounts in addition to Cincinnati private client business for our agencies' high net worth clients. This combined ratio was 106.9%, 0.7% -- percentage points better than last year despite an increase of 1.2 points from higher catastrophe losses. Excess and surplus lines grew net written premiums 15% and was also profitable with a combined ratio of 95.4%, up 3.2 percentage points from second quarter a year ago due to unfavorable reserve development. Both Cincinnati Re and Cincinnati Global were again very profitable and continue to reflect our efforts to diversify risk and further improve income stability. Cincinnati Re's combined ratio for the second quarter of 2024 was an excellent 70.1%. It grew net written premiums by 17%, bringing the overall six-month written premium for 2024 in line with 2023. Cincinnati Global's combined ratio was also excellent at 63.2%. While it grew net written premiums 2% for the first half of the year, second-quarter premiums were down 18%, reflecting pricing discipline in a very competitive market. Our life insurance subsidiary had an outstanding quarter including net income of $24 million and operating income growth of 26%. Term life insurance earned premiums grew 2%. I'll conclude with our primary measure of long-term financial performance, the value creation ratio. Our second-quarter 2024 VCR was 2.2%. Net income before investment gains or losses for the quarter contributed 1.6%. Higher overall valuation of our investment portfolio and other items contributed 0.6%. Now, chief financial officer, Mike Sewell, will add his comments to highlight other parts of our financial performance. Mike Sewell -- Chief Financial Officer Thank you, Steve, and thanks to all of you for joining us today. Investment income continued to grow, up 10% for the second quarter of 2024 compared with the same quarter in 2023. Dividend income was down 1%, or $1 million for the quarter, primarily due to two unusual items that totaled approximately $2 million. One was a holding with a June ex-dividend date in 2023 that moved to July 1st in 2024. The other was a holding that reduced its dividend rate by 53% after a spin-off transaction. Bond interest income grew 18% for the second quarter of this year. We again added fixed maturity securities to our investment portfolio with net purchases totaling $771 million for the first six months of the year. The second-quarter pre-tax average yield of 4.64% for the fixed maturity portfolio was up 30 basis points compared with last year. The average pre-tax yield for the total of purchased taxable and tax-exempt bonds during the second quarter of 2024 was 6.06%. Valuation changes in aggregate for the second quarter of 2024 were favorable for our equity portfolio, and unfavorable for our bond portfolio. Before tax effects, the net gain was $149 million for the equity portfolio, partially offset by a net loss of $93 million for the bond portfolio. At the end of the quarter, total investment portfolio net appreciated value was approximately $6.7 billion. The equity portfolio was in a net gain position of $7.4 billion, while the fixed maturity portfolio was in a net loss position of $700 million. Cash flow continued to benefit investment income in addition to a higher bond yields. Cash flow from operating activities for the first six months of 2024 was $1.1 billion, up 33% from a year ago. I'll move on to expense management where we always work to balance controlling expenses with making strategic investments in our business. The second quarter 2024 property casualty underwriting expense ratio was 0.5 percentage points higher than last year, reflecting higher levels of profit-sharing commissions for our agencies and employee-related expenses. Next, let me comment on loss reserves where our approach remains consistent and aims for net amounts in the upper half of the actuarially estimated range of net loss and loss expense reserves. As we do each quarter, we consider new information such as paid losses and case reserves, then we updated estimated ultimate losses and loss expenses by accident year and line of business. For the first six months of 2024, our net additions to property casualty loss expense reserves was $578 million including 506 million for the IBNR portion. During the second quarter, we experienced $40 million of property casualty net favorable reserve development on prior accident years that benefited the combined ratio by 1.9 percentage points. The commercial lines segment saw overall favorable reserve development of $29 million driven by workers compensation and commercial property, which more than offset the unfavorable development in commercial casualty. Commercial casualty was again the line of business having the largest amount of unfavorable reserve development with a total of $28 million for the quarter, or less than 1% of that line's year-end 2023 reserve balance. We released reserves in some recent accident years and added reserves totaling $51 million in aggregate for accident years prior to 2021, including $30 million for 2018 through 2020 due to case incurred losses emerging at amounts higher than we expected. The unfavorable amount reflects our slowing the release of IBNR reserves for some of those older accident years while adding to others. On an all-lines basis by exiting year, net reserve development for the first six months of 2024 included favorable $269 million for 2023, favorable $36 million for 2022, favorable $17 million for 2021, and an unfavorable $182 million in aggregate for accident years prior to 2021, with commercial casualty representing $167 million of the unfavorable $182 million. I'll conclude my comments with the capital management highlights, another area where we have a consistent long-term approach. We paid $125 million in dividends to shareholders during the second quarter of 2024. We also repurchased 395,000 shares at an average price per share of $116.33. We think our financial flexibility and our financial strength are both in excellent shape. Parent company cash and marketable securities at quarter end was nearly $5 billion. Debt to total capital contributed -- continued to be under 10%. And our quarter-end book value was at a record high $81.79 per share with $12.8 billion of GAAP consolidated shareholders' equity providing plenty of capacity for profitable growth of our insurance operations. Now, I'll turn the call back over to Steve. Steve Spray -- President and Chief Executive Officer Thanks, Mike. Before we move on to questions, I'd like to share some additional observations based on my first few months as CEO. I've spoken with many of our agents and associates and they share my high level of confidence in the future of this company. In the first six months of this year, we've achieved a combined ratio of 96.1%. That makes 12.5 consecutive years of underwriting profit, a core loss ratio that continues to improve, growth in net written premiums of 14% with investment income up 13%. We've set the stage for 64 years of increasing dividends to shareholders. In the most challenging market of my career, our balance sheet allows us to lean in and grow with our agents, and I'm really excited about where we're headed. As a reminder, with Mike and me today are Steve Johnston, Steve Soloria, Mark Schambow, and Theresa Hoffer. Jason, please open the call for questions. Operator Questions & Answers: |

Cincinnati-financial